Mortgages in the Netherlands – Everything You Need to Know About Dutch Mortgages

Categories: Housing

If you’re looking at buying a property in The Netherlands, having a mortgage is pretty much essential, unless you happen to have several hundred thousand euros sitting around in your bank account. Even if you are blessed with such resources, hanging onto that cash to grow your wealth with other investments is never a bad idea.

In this article, with the help of our partners, The Expat Specialist, we’ll delve into the world of Dutch mortgages and discuss how to secure one in the Netherlands today.

What is a Mortgage?

A mortgage is essentially a loan you get from a bank or lender to buy a house or investment property. They lend you the money. You pay them back the full amount, plus interest, in monthly installments. A mortgage payment generally has two parts:

- The principal or equity (Aflossing) – the amount you borrowed

- Interest (Rente) – the amount the bank or lender charges to borrow the money

These payments are divided so that the property is paid off by the end of the mortgage term, which is usually around 30 years. Lenders will often let you decide the fixed interest rate period of the mortgage (it could be 10, 15, 20, or 30 years), which means that midway through your mortgage term, you have the opportunity to change lender providers or change the interest rate. Keep in mind that a change of interest rate could be a good thing or a bad thing depending on the one set by the European Central Bank.

Where Can You Get a Mortgage in the Netherlands?

Mortgages can be secured either through a bank or a mortgage broker. The advantages of going through a broker allow you to compare different lenders and see what the options are. A good mortgage broker will understand your needs and match you to the best mortgages for expats based on your situation.

The advantage of going to the bank is that you don’t have to pay a mortgage broker, although they obviously won’t provide you with the offers of their competitors (other lenders) that may be better suited to you.

Note: Mortgage brokers in the Netherlands are not allowed to receive commissions or fees from lenders when they secure your business. This is why you have to pay the fee to the mortgage broker yourself because they represent you, not the lenders or banks. This is a requirement of the Dutch Authority for the Financial Markets (AFM).

How to Apply for a Mortgage in the Netherlands

In most cases, you will start the process by arranging a consultation with a mortgage provider and/or broker. This will help define your budget and understand whether you meet the requirements. Then comes the exciting part – hunting for a property. You can do this independently or with a real estate agent (see our list of real estate agents and property management in the Netherlands). Once you’ve found your ideal home, it’s time to make an offer. If accepted, you’ll meet the seller at a notary’s office to sign the purchase agreement and from there you can apply for a mortgage.

As expected, there are a number of requirements. Expats in particular must:

- Live in the Netherlands (although your work can be abroad)

- Earn a salary in Euros (if you get paid in a foreign currency, a Dutch lender won’t give you a mortgage)

- Have a BSN number and residence permit (if you’re not an EU citizen)

If you are buying together as a couple, your partner must live in the Netherlands too, even if you’re purchasing the property on just your own salary.

Those on a temporary contract or working as a researcher or Ph.D. student at a university can only get a mortgage in the Netherlands if their employer states that their position will become permanent.

If you’re self-employed or starting a business in the Netherlands, you’ll need to be able to present an income history of at least three years (although some lenders may only ask for 1 year). Your net profit will be used to calculate the maximum mortgage available. If your numbers are increasing, a lender will use the average net profit. If they’re decreasing, the lower figure will be used to calculate your mortgage.

The Most Awesome Things About Mortgages in the Netherlands:

Mortgage Interest Deduction

Contrary to a lot of other countries, the Netherlands offers homeowners the unique ability to deduct the interest paid on their mortgage from their income. In other words, interest paid on a mortgage is tax-deductible. It’s known as ‘Hypotheekrenteaftrek’, yet it is only available on annuity and linear mortgages (see below).

You’ll also hear about ‘brutto’ (gross) mortgage payments or ‘netto’ (net) mortgage payments. The basic difference comes down to the tax deductions you apply due to interest. You can actually get the tax refund on a monthly basis or choose to receive it as a lump sum when you file your income tax return the following year.

No Down Payment

Yes, you can get a mortgage for 100% of the value of the property without providing a down payment in the Netherlands. There are, however, some things to bear in mind.

You will still need savings. We know, there’s always a catch, but if you’re looking to build up your money pot, you can always check out these great tips on how to save money in the Netherlands. When you’re buying a property, there are a variety of different costs you’ll have to pay related to the transfer of it. These include:

- Property Transfer Tax (you pay 2% of the purchase price)

- Notary Fee

- Broker Fee

- Appraisal Costs

and, if applicable:

- Real Estate Agent Fee

- A Survey of the Property

- National Mortgage Guarantee (see below)

- Bank guarantee

Overall, these costs tend to add up to around 5-6% of the purchase price. So, if your prospective property is worth €400,000, that’s €20,000-€24,000 you’ll have to fork out yourself.

Another thing to bear in mind is that overbidding is extremely common in the larger cities of the Netherlands. That is, offers going above and beyond the asking price. You may find yourself having to overbid your dream property as a result of such a competitive market. As you can only borrow 100% of a property’s market value, you will have to pay the amount you overbid out of your own pocket as well.

How Much Can I Borrow?

The amount you can borrow depends on your income, financial situation, and employment contract. As a rule of thumb, banks will lend you about 5 times the amount of your gross yearly income. The key is to speak to a mortgage broker who can advise you. Check out this Dutch mortgage calculator to get a rough estimate of what you can borrow.

Beware: Banks and lenders will not lend you more than the value of the property.

Example: You place an offer on a house which has been evaluated at €400.000 and your salary allows you a mortgage of €450.000. The lender will most likely not cover the other €50.000.

Types of Mortgages in The Netherlands

There are a number of different Dutch mortgages you can choose from in the Netherlands, and they all have their advantages and disadvantages. At the end of the day, your mortgage broker or advisor will be able to advise you on which mortgage is right for you. Remember that financial advisors are regulated by the Dutch Authority for the Financial Markets (AFM) – the strictest and most reputable financial authority in Europe.

Here’s a quick rundown of the kinds of mortgages on offer in the Netherlands:

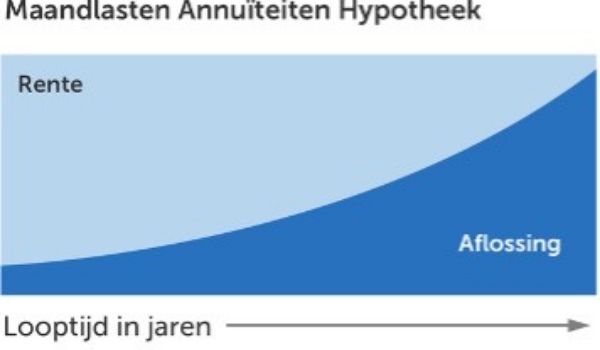

Annuity Mortgage – Annuiteit Hyptheek (Most Common for Expats)

An annuity mortgage contains both interest and principal payments. In the beginning, a large amount of the payments you make go towards interest. A small amount goes towards the actual loan repayment. As you reduce your debt, the less interest you’ll pay. In the final years of your mortgage, the payments are reversed, so you’ll be paying higher principal payments and lower interest payments.

So, because the majority of mortgage payments, in the beginning, are predominantly interest, the tax deductions are higher, making for lower net monthly payments in the beginning. As the years’ progress, your net mortgage payments will tend to rise (assuming you don’t put any lump sum payments towards the principal) because the interest portion of what you pay per month decreases, so the tax deduction decreases.

Initially, you pay more interest and over time the percentage of the principal amount paid steadily gets bigger each month, as illustrated by the graph below:

Source: Consumentenbond.nl

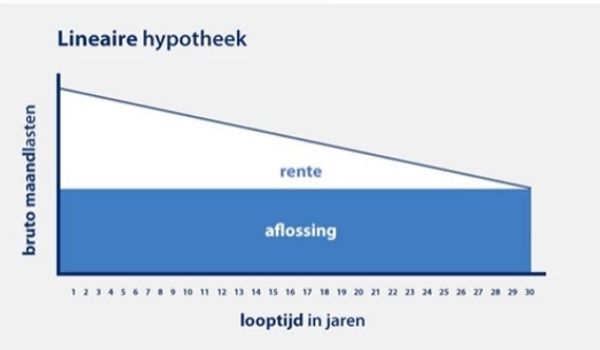

Linear Mortgage – Lineaire Hypotheek

A linear mortgage is also an option for expats. It differs from the annuity mortgage because the amount of principal paid is the same every month for the duration of the mortgage. The interest portion of the mortgage decreases in a linear fashion over the years. Both the gross and net mortgage decrease over time. The graph below illustrates how your payments will look over time.

Source: hypotheker.nl

Interest-Only Mortgage – Aflossingsvrije Hypotheek

The interest-only mortgage is exactly that – you only pay the interest for the term of the mortgage and the capital is usually to be paid at the end of the term or when the house is sold. Of course, some lenders will give you the option to inject payments at your convenience to bring down the overall debt. The benefits of the interest-only mortgage are that the monthly payments tend to be less because you’re only paying interest. Keep in mind that there are risks (as with any time you borrow money). If you decide to sell, you may not get enough to pay back the entire debt (because of market conditions, for example). In the event that you decide to hold the property for the duration of the mortgage, you will need to pay off the entire amount at the end of the term (generally 30 years).

Other types of Mortgages You May Come Across:

- Savings mortgage (spaarhypotheek)

- Investment mortgage (beleggingshypotheek)

- Credit mortgage (krediethypotheek)

- Life insurance mortgage (levenhypotheek)

- Hybrid mortgage (hybride hypotheek)

Terms and Conditions to Consider When Applying for Your Mortgage:

Renting Out Your Property

If your mortgage is on your principal residence, many lenders will not allow you to rent out your property. This is because your mortgage would not be classified as a buy-to-let mortgage. Buy-to-let mortgages generally have large down payments associated with their terms and conditions (20-30%). Keep in mind, however, that lenders will allow you to not live in your place for 2-5 years as they understand people move abroad. As a good rule of thumb – pay your mortgage. They are usually auto deducted from your bank account anyhow, just make sure it has money in it to cover the mortgage at the time of debit.

Click the link to find out more information on renting out your property or house in the Netherlands if this is something you are considering.

Note: Buy-to-let investors pay a higher property transfer tax of 8% as of January 2021.

Principal Payments

Some lenders will restrict how much principal you can pay back in lump sums. It’s not uncommon for that to be 10% of the mortgage per year.

Interest Rates for Mortgages as of 2021

Like anywhere, interest rates for mortgages are influenced by the lender, the duration of the fixed interest period, and the risk level the lender will calculate. Interest rates in 2021 are at historic lows. Below is a rough idea of the rates you can expect to pay based on a 100% loan-to-value from the major banks in the Netherlands.

- 5-year fixed rate: 0,75% – 1,27%

- 10-year fixed rate: 0,86% – 1,38%

- 20-year fixed rate: 1,17 – 1,73%

Need Help?

Let’s face it, mortgages can be complicated and expensive. Fortunately, there are systems you can use to help you out along the way.

The National Mortgage Guarantee (NHG)

The National Mortgage Guarantee is a unique governmental scheme that guarantees repayments for smaller mortgages. If you’re unable to work due to circumstances beyond your control (such as you lost your job, you become disabled, you get divorced or your partner dies), the NHG will ensure your lender receives the correct payment. As such, this safety net allows lenders to offer a lower interest rate and thus lower monthly payments.

Certain conditions do apply. In 2021, the total amount of the mortgage cannot exceed €325,000; the maximum interest-only percentage is 50%; an NHG-backed mortgage can only be taken out on a maximum 30-year term.

Parental Gift

If your family has the means and you’re between 18 and 40 years old, you can receive up to €105,302 as a tax-free gift. This can be used towards mortgage payments, purchasing fees, and/or renovations.

No Transfer Tax

Great news if you’re a first-time buyer between the ages of 18 and 35 years old. As of April 1st, 2021, you will not need to pay the 2% transfer tax if your property is worth less than €400,000.

Note: First-time homebuyers between 18-35-year-old are exempt from paying the 2% property transfer tax on a maximum purchase price of € 400.000. When the purchase price is over € 400.000, the 2% transfer tax applies.

Conclusion

There’s a lot to think about when it comes to mortgages in another country. Assess your options and take time to think about things such as location, the condition of the building, and the long-term benefits and drawbacks you may face. Don’t be afraid to seek advice from experts like The Expat Specialist, who’ll help you every step of the way so you can find your new home and enjoy it for years to come.